Hi folks, today I am writing about a February 2023 stock teaser presentation by The Oxford Club’s Marc Lichtenfeld that centers around his “#1 oil and gas royalty” stock.

According to Lichtenfeld, this is a way to “collect monthly income over and over again” while also “banking huge capital gains.”

“Today, I’ll show you my #1 play to profit from the oil and gas surge in 2023.

“It’s a way to…

“Collect monthly income over and over again… for life…

“While banking huge capital gains.

“The average return on this unusual class of investments was 196% last year…

“And I believe that my pick is poised to see the same profit potential this year.”

Source: https://web.archive.org/web/20230320041319/https://pro.oxfordclub.com/p/OILTO79BRKLT2YRDSTOT/NBRKZ306/Full

If you’ve seen the pitch, you’ll know that he doesn’t reveal his pick because he wants you to buy a subscription to his Oxford Income Letter service to find out.

I looked into the clues he shared about this company, though, and think I know what his oil and gas pick is. I also managed to uncover a second oil stock he teased.

So if you want to know what he’s spruiking, read on!

Overview of Lichtenfeld’s 2023 Oil and Gas Prediction

According to his recent presentation, Marc Lichtenfeld believes that a “major shift” occurring in the oil market will cause oil prices to “leap far higher from today’s levels.” He even went as far as to predict that we’re entering the “greatest oil bull market since the 1970s.”

“I believe there’s a major shift that’s occurring in the oil market.

“I’ll tell you more in a minute, but I believe it will cause prices to leap far higher from today’s levels… and lead to the biggest bull market we’ve ever seen in fossil fuels.”

[…]

“I believe we’re entering the greatest oil bull market since the 1970s.”

Why is he so bullish? From what I can tell, the reason Lichtenfeld is bullish on oil is that his research suggests that “supply is down” while demand is “surging.”

Here’s how Lichtenfeld himself puts it:

“In short…

“Supply is down.

“And reserves are low.

“All while demand is surging.

“So it’s inevitable that oil prices are going to rise dramatically.”

There is more nuance to his thesis than that, but that’s the gist of it.

Only time will tell if what he’s predicting plays out or not.

And of course, there is no guarantee that the price of oil will rise, much less that any one company will benefit as a result.

But I do think Lichtenfeld made some interesting points in his pitch regarding oil in general. And I wanted to know what company he was talking about.

So I did some digging to see what I could find…

Marc Lichtenfeld’s “#1 Oil and Gas Royalty” Stock for 2023 Revealed

As you may have gathered by now, Lichtenfeld’s oil and gas pick is a royalty company.

What’s that?

In short, these are companies that own the rights to different oil and gas fields and collect a “royalty stream” (aka they earn revenue) by letting other companies do the exploration and drilling, etc, on land they own.

Here’s how Lichtenfeld puts it:

“‘Oil and gas royalties’ are a backdoor way to get paid over and over again from oil and gas properties.

“You get to bypass all the normal costs of doing business, like exploration, hiring rig workers, buying machinery, and bringing your oil and gas to market.

“Instead, you simply collect incredible royalty streams for owning a very valuable asset… the oil or gas field.

“It’s the ultimate passive income investment.”

Similar to a different royalty stock he teased a while back, Lichtenfeld highlighted all of the good points about royalty companies in the presentation.

But like any investment, there are risks to consider.

As Lichtenfled points out, these companies don’t have the same operational expenses as a typical oil and gas company. So they can potentially be highly profitable. But if they’re buying up lots of land with debt, for example, and the interest on that debt rises (say, due to the Fed raising rates), then their profitability can be negatively impacted.

Not to mention, they don’t have control over the operational side of things, so their business is reliant on what a third-party company is doing.

And they are often heavily invested in one sector (like oil or gold).

I’m not saying royalties are a bad idea. Not at all. I don’t give investment advice on this blog (or any blog), so what you invest in is totally up to you.

But I did want to point out that there are always two sides to consider with this sort of thing, and these sales pitches rarely discuss the negatives, as they want your subscription.

Anyway, with all that said… here are the clues Lichtenfeld shared about his pick:

“I’ve found the single greatest royalty stream to directly tap into the Permian Basin’s huge growth.

“Unlike with Occidental, you’re not investing in a high-capital company that needs to drill, extract, transport or store any product.

“Rather, you simply collect royalties on the oil and gas that comes out of this superstar basin.

“It’s a win-win.

“You get profit potential… while the oil companies take the risk.

“This single royalty lets you profit from over 380,000 acres in prime oil and gas fields.

“Revenue is at its highest level in three years, as are earnings.

“It has no debt, has $11 million in cash and pays out its earnings back to shareholders, hence the sky-high yield.

“Quarterly revenue growth is up a staggering 717%…

“Over the last year, it’s brought in $42 million.”

[…]

“And you can own a piece of this royalty stream for just $25.”

What stock is he teasing here?

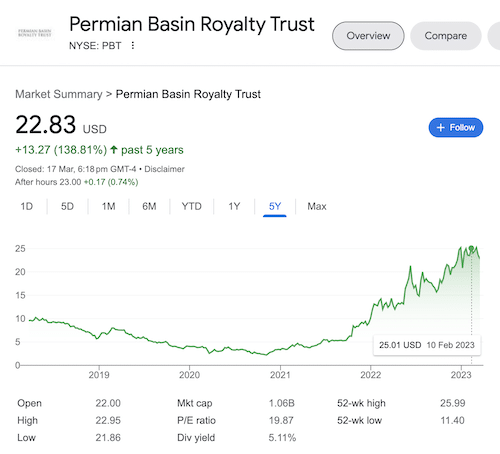

Based on the above clues, I think Lichtenfeld’s “#1 oil and gas royalty” stock pick is the Permian Basin Royalty Trust (ticker: PBT).

PBT is a Dallas-based oil and natural gas royalty trust, and while I can’t be certain, this company seems to match Lichtenfeld’s clues very closely.

It’s worth noting that Lichtenfeld appears to have used the company’s Q3 2022 report when citing the above numbers, as this is the latest earnings report released on the company website as of writing, and the numbers in that report line up with what he said.

For example, according to Permian Basin Royalty Trust’s Q3 2022 report:

- The company’s Q3 revenue for 2022 was $27,323,759, and its Q3 revenue for 2021 was $3,344,086, which represents roughly 717% in revenue growth.

- The company’s “cash and short-term investments” totaled just over $11.5 million leading up to September 2022.

Furthermore, according to this page on Yahoo Finance, the company earned just over $42 million in the 12-month period leading up to September 2022.

So, while I have no idea if it’s a good investment or not, PBT looks like a match based on the clues Lichtenfeld shared in the presentation.

He also teased two other companies.

One was a gold stock that I wasn’t able to uncover due to limited clues, and another was an oil and gas company, which was an easy one to solve.

So let’s discuss that now.

Uncovering Lichtenfeld Second Pick: “The World’s Leading Oil and Gas Partnership”

Here’s what Lichtenfeld said about his second oil and gas pick:

“Just like my #1 royalty opportunity, this is NOT a regular stock.

“Instead, you become a PARTNER in a company that owns over 50,000 miles of oil and gas pipelines across the country.

“And oil producers like Chevron, Exxon Mobil and Occidental use these pipelines to get their crude to market.

“This company is like a toll collector for these big oil and gas companies.

“They use its pipelines to transport their products… And pay the toll each time they do.”

[…]

“Over the past 12 months, this company has banked $55 billion in revenues…

“And it just raised its dividend to a whopping 7.45% annual yield.

“What’s more, it’s raised this dividend every year since 1998.”

What’s this one?

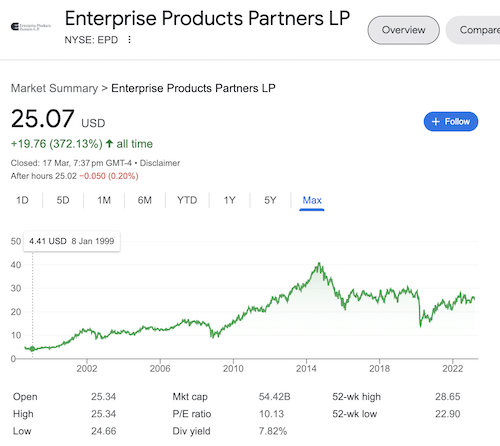

As soon as I saw the clue about how the company owns over 50,000 miles of oil and gas pipelines across the U.S., I knew Lichtenfeld was talking about Enterprise Products Partners LP (ticker: EPD), as this is a company I’ve seen teased numerous times before.

Not only does this company own over 50,000 miles of pipeline, but it has increased its dividend since 1998, which is currently sitting at around 7.8%.

So, this one looks like a match as well.

Bottom Line

Nobody knows what will happen with the price of oil or the companies operating in this space, but I’ve seen quite a few stock pickers and investment analysts calling for higher oil prices lately. And for the most part, their predictions seem similar to what Lichtenfeld talked about (lack of supply and increased demand, despite the push toward renewables).

I don’t know what stocks are a good bet, nor do I make those types of predictions. But at least now you don’t have to fork out $49 for Lichtenfeld’s Oxford Income Letter service just to find out what his top oil and gas pick is (assuming my guess is right, of course).

I am a member of that service, so I could literally just log in to my account and find out what it is, but out of respect for the fact that it’s a paid service, I didn’t do that.

That said, if you want to know more about his service before deciding if it’s a good idea to join, I would recommend seeing my Oxford Income Letter review. In it, I discuss what the service is, how it works, and how Lichtenfeld’s picks have worked out.

So, that may help you decide if it’s a good idea to try or not.

Anyway, that’s it from me.

I hope you enjoyed the article, and thanks for reading!

I would like to know if these royalty stock can be held in a TFSA account and if so what is the company ?

Rober

Hi. Marc Lichtenfeld has been on again after using his top rated software.His tip was a

7 dollar company supplying tooling to the energy sector.Revenue and earnings going

like a rocket no debt and under the radar.Next earnings date July 26 th 2023 he says he’ll be buying the day before.Had a look couldn’t find anything,didn’t try earnings date.

Thanks for all your hard work.

Hey Peter, do you have a link to that presentation by chance?

Garret Baldwin was on talking about Exxon trying to buy out Pioneer (fracking operation). Said that if managed Exxon’s cost per barrel falls to 15 dollars.Said would

set of a buy out frenzy named 1 he thought would be good and gave clues at fast speed on 4 others.Exxon still hoping.

Thanks for the heads up. I think I just found the teaser you’re referring to. Will take a look and see what I can find.

What stock did U find

Thanks for the info! Really has been helpful.

My pleasure John, glad it helped!