Hello, and welcome. Today we’ll be discussing a presentation from Bob Carlson that claims to help you create a “Second Social Security check.”

According to Mr. Carlson, depending on your situation, it could pay you between a few hundred to a few thousand dollars each month, in addition to your regular social security check.

Even if the stock market crashes or the economy nosedives.

Sounds good, but is it the real deal?

Based on my research, it’s not a scam. However, to get the full details on earning money from Mr. Carlson’s “Second Social Security check” strategy, you must join his Retirement Watch Spotlight Series. And this costs either $139 for one year or $199 for two years.

So, in this article, I’ll shed some light on what this “check” is all about and how Retirement Watch Spotlight works to help you decide if it’s worthwhile.

Can You Really Get a “Second Social Security” Check?

In a presentation on the Retirement Watch website, Bob Carlson states that you can create a “Second Social Security” check that could pay you a “guaranteed income for life.”

According to Mr. Carlson, it’s an “excellent alternative to IRAs and 401(k)s” because you can get a “steady, dependable, and predictable monthly income for life,” regardless of what’s going on in the market. Which he says means you can “end any worries about outliving your money.”

What he talked about in the presentation reminded me of a different program I wrote about recently from Tim Plaehn, called the 36-Month Accelerated Income Plan.

In short, Mr. Plaehn suggests that two of the biggest fears retirees face are running out of money during retirement and a stock market crash. Which makes a lot of sense since either of these things could potentially ruin an otherwise enjoyable retirement.

And while the solution Mr. Carlson offers is different from that of Mr. Plaehn, these are more or less the two main issues he addresses within his presentation.

Specifically, he says that the “Second Social Security check” can help you “enjoy a guaranteed lifetime income.” And that it doesn’t matter if the stock market crashes, the economy nosedives, or interest rates go up or down.

In other words, he more or less suggests it’s “bulletproof.”

He also points out why it’s so important to pay attention now. According to Mr. Carlson, the “U.S. Social Security will be underwater” starting in 2022 and will run out of money altogether 12 years later. If true, that’s a bit concerning (to say the least).

Is what he says true?

According to an August 2021 article on CNBC, “The Social Security trust fund most Americans rely on for their retirement will run out of money in 12 years.”

So it seems as though what he says about Social Security running out of money is true. In fact, it looks like it could happen a year earlier than he suggests in the presentation. Of course, that doesn’t mean it will happen, but Mr. Carlson is basing what he said on actual estimates.

What is this “Second Social Security” check?

And is it legitimate?

Well, first and foremost, Mr. Carlson is NOT talking about getting an actual social security check. He might call it a “Second Social Security check,” but that is not what he’s referring to.

Instead, it seems as though he’s referring to something called annuities.

He doesn’t say this in the presentation, so I am not 100% sure, but it does appear that when he says “Second Social Security check,” he’s referring to some type of annuity.

Why do I say this?

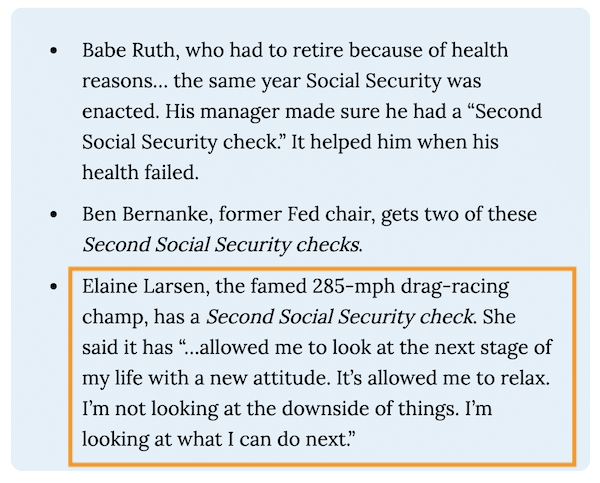

Because first of all, he lists three well-known people (Babe Ruth, Ben Bernanke, and Elaine Larson) who supposedly benefited from a “Second Social Security” check:

I did some Googling, and the common thread is that each of these people invested in annuities. And the quote Mr. Carlson shared from Elaine Larsen (above) was taken from an article in the Retirement Income Journal that shows she was referring to an annuity.

Here’s the quote (notice the first few words and compare it to above):

The annuity has allowed me to look at the next stage of my life with a new attitude. It’s allowed me to relax. I’m not looking at the downside of things. I’m looking at what I can do next.

Source: retirementincomejournal.com

What’s an annuity? I’m not a financial advisor, so it’s best to speak to an expert and do your own research on this topic.

However, with that said, according to Investopedia, an annuity is an insurance contract issued and distributed by financial institutions that offers a guaranteed income stream. And they can “provide a steady cash flow for people during their retirement years.”

The page I just linked to on the Investopedia website does an excellent job of breaking down what annuities are, how they work, different types of annuities, and so on.

So it’s well worth a read if you want to learn more.

I also found a Youtube video explaining how different types of annuities exist and different financial institutions offer them that you might find helpful:

So, based on my research, it seems as though annuities line up with what Bob Carlson talks about in the presentation. However, assuming this is what he’s talking about, it’s still unclear what type of annuity he’s referring to. Much less the specifics around it.

How do you get all the details?

Bob Carlson says he created a presentation called “How to Generate Guaranteed Lifetime Income” that shows you everything you need to know.

And to access that presentation, you need to join the Retirement Watch Spotlight Series. So let’s look at what this is all about and how it works to give you a better idea of what to expect.

What Is the Retirement Watch Spotlight Series?

The Retirement Watch Spotlight Series is a monthly video presentation where Bob Carlson “spotlights” the latest challenges facing retirees and provides actionable tips on overcoming these. He says it’s best to think of it as the “60 minutes” for retirees.

That’s why, every month, I spotlight the latest changes – along with the biggest retirement issues of the day – and break them down into a plain-English, easy-to-understand video presentation.

And, at the end of each presentation, you get helpful action steps for each crucial point.

Think of it as the “60 Minutes” for retirees.

According to Mr. Carlson, the Retirement Watch Spotlight Series covers topics related to IRAs and 401(k), minimizing taxes, protecting and growing wealth for retirement, and more.

He likens it to “having a top financial retirement advisor” around the clock who keeps updated on the latest news and regulations impacting retirement.

All in all, it looks like a pretty good resource for retirees.

How much does it cost?

There are two membership options for the What Is the Retirement Watch Spotlight Series.

The first option costs $139 for one year.

This gives you access to 12 monthly video presentations, the “How to Generate Guaranteed Lifetime Income” presentation that walks you through Mr. Carlson’s “Second Social Security” check strategy we discussed earlier, and the following two bonus reports:

- The IRA Investment Guide: A Road Map for Avoiding the Traps and Penalties for IRA Investments

- Bob Carlson’s Guide to Inheriting IRAs

The second option costs $199 for two years.

This option costs you more upfront but works out cheaper in the long run. And it appears as though you get access to the same two bonus reports listed above.

Can you get a refund if you’re not satisfied with the service? No, according to the company website, there are no refunds available with this service.

Recommended: Go here to see my #1 rated stock advisory of 2024

Who Is Bob Carlson?

Bob Carlson is a former accountant and attorney, and he’s one of the foremost experts on retirement in the financial education space.

According to his bio on the Retirement Watch website, Mr. Carlson started writing financial newsletters in the 1980s. In particular, he was the editor of a newsletter called Tax-Wise Money.

This led him to write a book called Retirement Tax Guide, and then in 1991, he launched a retirement-focused monthly newsletter called Retirement Watch, which is still around today.

In fact, not only is it still around, Retirement Watch is one of the most popular and well-regarded newsletters in the retirement niche. It’s also a great compliment to the Retirement Watch Spotlight Series.

And I say this because, while the Spotlight Series is a monthly video focused on retirement, the Retirement Watch newsletter is a monthly write-up from Bob Carlson detailing his latest research, insights, and recommendations. So the two go hand in hand.

You can see my Retirement Watch newsletter review to learn more. In that article, I detail how it works, what you get if you sign up, how much it costs, etc. So you might find it helpful.

Aside from Retirement Watch, Bob Carlson is an accomplished author, senior contributor to Forbes and has managed billions of dollars for pension funds over the years. So he’s not just a newsletter writer; he’s an expert when it comes to retirement investing.

Bottom Line

The “Second Social Security check” Bob Carlson speaks about on the Retirement Watch website isn’t really a second check you receive from Social Security. Instead, based on my research, it appears to be a retirement strategy centering around annuities.

Mr. Carlson details his retirement strategy in a video presentation called “How to Generate Guaranteed Lifetime Income,” which you can access by joining the Retirement Watch Spotlight Series for either $139 or $199. So that’s the best way to find out for sure and get all the info.

Is it the real deal?

I’m not at the stage of entering retirement myself, so I didn’t join Retirement Watch Spotlight Series, and therefore can’t say for sure how worthwhile it is.

However, based on everything I’ve seen, Bob Carlson is a genuine expert on retirement, and Retirement Watch has been around for over 30 years. So, while it might pay to take the whole “Second Social Security” thing with a pinch of salt, I don’t believe it’s a scam.

That said, there are always risks when it comes to investing.

So even though Mr. Carlson’s strategy might aim to help you earn “guaranteed income for life,” there is always some type of risk involved. This is why it’s essential to do your own research before deciding anything, to figure out what is best for you and your circumstances.

Anyway, whatever you decide, I hope you found this post helpful.

And thanks for reading.

Please note: By submitting a comment using the above comment form, you confirm that you agree with the storage and handling of your data by this site as detailed in our Privacy Policy.